Introduction

As the crisis of the twenty-first century looms over us, the European Union has decided to adopt the Carbon Border Adjustment Mechanism (CBAM). The Union currently has a compliance model based on the cap-and-trade principle, the European Union Emissions Trading System. Parallelly, India has been developing its own instruments to tackle climate change. CBAM introduces regulations pertaining to the pricing of implicit embedded emissions in imports, requiring importers to obtain CBAM certificates corresponding to the level of greenhouse gasses in the product. Although there have been discussions regarding the nature of the levy, cooperation by the EU with its trade partners is a critical question to be explored in light of the Most-Favoured Nation (MFN) obligation. The article address this question arguing that the European Union’s implementation of the CBAM must consider its implications under WTO obligations, particularly the MFN principle. It emphasizes the importance of international cooperation and recognition of diverse climate policies, by analysing India’s case .

MFN Obligation

CBAM has triggered fears of green protectionism and questions regarding its WTO compatibility, calling for an analysis under one of the cornerstone obligations of the GATT 1994: Most-Favoured Nation treatment (MFN). Green protectionism is commonly understood as an addition of discriminatory or exceedingly trade-restrictive elements to the design of an environmental policy. Encapsulated in Article I of the GATT, MFN requires any advantage extended to any particular nation, be extended to all other members. The analysis must be between ‘like products’, and by incorporating paragraphs 2 and 4 of Article III of the GATT, it applies to not just border measures but internal measures as well.

The panel in EC- Bananas III gave a broad interpretation of an ‘advantage’ and considered it to be any measure that creates “more favourable competitive opportunities” or affects the commercial relationship between products of different origins. In US – Tuna II, following the rationale in EC – Seal Products (2014), the Appellate Body when adjudicating upon the consistency of the amended dolphin-safe labelling measure with Articles I:1 and III:4, focused on whether the measure modified conditions of competition in the US market to the simultaneous disadvantage of Mexican tuna products vis-à-vis US tuna products or tuna products originating anywhere. An advantage in the context of CBAM, would also require a review of the domestic comparator, EU ETS.

International Cooperation

Considering domestic socio-economic realities, governments around the world have undertaken their own policies to combat climate change. To allow for this, under Article 9 of the instrument, the number of CBAM certificates to be obtained can be reduced if an effective carbon price was paid in the country of origin. The domestic comparator: EU ETS, established in 2005, covers all EFTA nations, and is particularly applicable to certain heavily polluting industries. Here, carbon allowances are treated as a commodity that can be auctioned or traded, offering the firm the right to pollute to the extent of their individual allowances. Consequently, the calculation of the price of CBAM certificates is set to reflect the EU ETS prices. As per a report of the German Emissions Trading Authority, the framework of EU ETS allows for the linkage of emissions trading systems, both directly and indirectly; the former being distinguished further into unilateral and multilateral agreements.

The Swiss ETS and EU ETS were linked in 2020, and it is the first international linkage offering benefits for both parties through mutual recognition of allowances. Now the technocratic exercises that importers would have to comply with will have to be comparable with those under the EU ETS, which would otherwise lead to an absence of level-pegging as construed by the MFN Principle between the goods from the linked countries and other members. In addition to this linkage there has been bilateral cooperation with China for an Emission Trading network, policy dialogue, joint research and beyond in China; through the project – EU China ETS. Which is also being funded by the European Union. Over the years, China has emerged as the largest origin for EU imports, therefore, it cannot be viewed as not having a nexus with trade.

In EC- Bananas III it was determined that the procedural and administrative requirements for bananas originating in countries other than African, Caribbean, and Pacific (ACP) states, were different and significantly higher than those required for importing ACP bananas. Similarly, the flexibility offered by the EU to its trading partners would have to be considered in addressing the legality of CBAM under the WTO regime. The administrative exercises would have to be comparable between the EU ETS and CBAM. If not, the linkages of the systems and bilateral cooperation could be viewed as an advantage.

General Exceptions under the GATT

Exceptions exist in the GATT to justify its violations and some of the most commonly cited exceptions are those of Article XX(b) and Article XX(g). Under Article XX the analysis first calls for a determination of the specific paragraph cited and then the requirements of the chapeau have to be analysed. In US- Shrimp when analysing the application of the measure under the chapeau, both the panel and the appellate body stressed upon the lack of multilateral or bilateral cooperation on behalf of the U.S with the complainants, while having a regional international agreement -The Inter American Convention with South American countries (as a result of which they were not subject to the trade restrictiveness of the measure). It was concluded that the existence of the convention proved that there was a less trade-restrictive manner to achieve the objective of the measure.

Resorting to diplomacy and actively engaging with certain countries and not others was held to be unjustifiable discrimination. In addition to this it was laid out in US- Gasoline, that the freedom of WTO Members “to adopt their own policies aimed at protecting the environment as long as, in so doing, they fulfil their obligations and respect the rights of other Members under the WTO Agreement.” Parallels can be drawn in this scenario as well; if it is easier for countries with an emissions trading system to link the same, they should be given the opportunity to do so. If they follow mechanisms different from carbon pricing and emissions trading such instruments should also be catered to.

The Indian Context

Until recently, energy efficiency was the crux of India’s low-carbon development strategy, and a crucial regulatory instrument in this regard is the Perform, Achieve, Trade (PAT) scheme. The objective is to reduce Specific Energy Consumption (SEC) in energy intensive industries by issuing Energy Savings Certificates or EScerts, when energy consumption is lower than the prescribed norm. Excess certificates can then be traded at the Power Exchanges- India Energy Exchange and Power Exchange of India Limited. However, they are not denominated in terms of GHG reductions, which is the de-facto trading unit of most compliance based as well as voluntary carbon markets around the world.

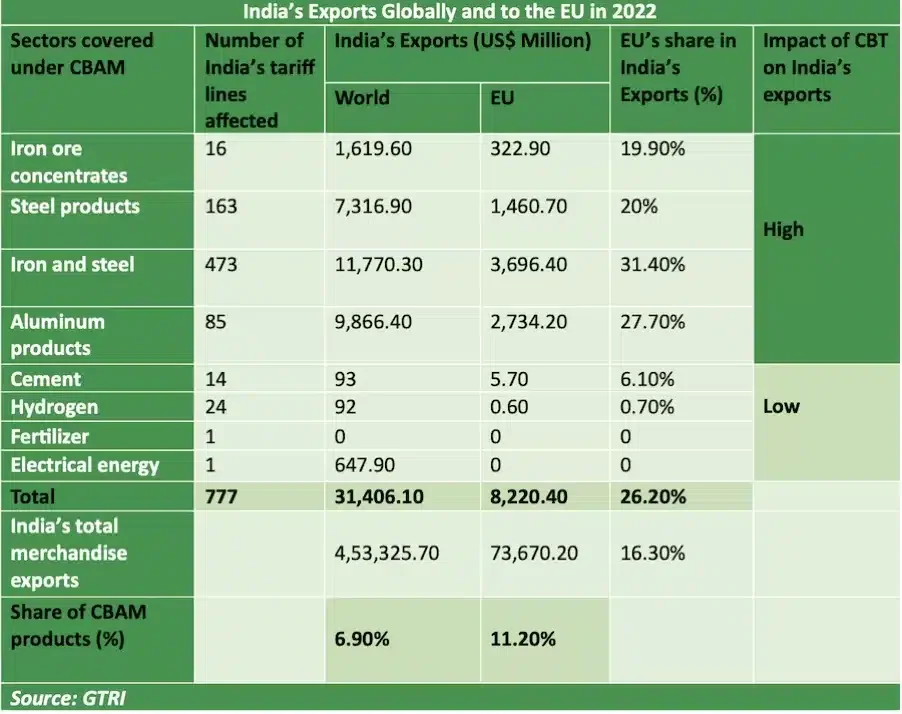

Currently there are two trading schemes available in the energy sector – Renewable Energy Certificate under the Electricity Act, 2003 and the Energy Savings Certificate under the Energy Conservation Act, 2001. The amendments made in 2022 to the latter, envisions a carbon trading market by adding for carbon credit certification. Indian Commerce and Industry Minister Piyush Goyal who although does not believe in the long-term sustenance of CBAM, has been pushing for the recognition of the newly designed Indian Carbon Credit Trading System (CCTS). In order to comply with the instrument, since, EU is the destination for one-fourth of India’s energy-intensive products such as iron ore concentrates, steel, aluminium, and cement.

Conclusion

Varying levels and different kinds of cooperation between its trading partners should be factored in when analysing the EU’s obligation under Article I of the GATT. Further the Appellate Body in US- Shrimp, when analysing the chapeau of Article XX of the GATT, opined that, sovereign states should adopt effective measures for the protection of endangered species, but the measure should not constitute “arbitrary and unjustifiable discrimination between Members of the WTO”. India favours reducing emissions through policies based on energy savings but has developed an instrument to be on par with its trading partner, and these efforts should be recognised at the earliest. Selective cooperation with policies aimed at combating climate change would only strengthen fears of green protectionism and a case for violations under the GATT, for competition will be tweaked to the disadvantage of countries that have adopted strategies different from those promoted by the EU.

Nikita Lal is an LLM Candidate in International Economic Law at European Public Law Organization (EPLO) Athens, Greece.

The image is AI generated using Adobe Firefly.

{kind=link}